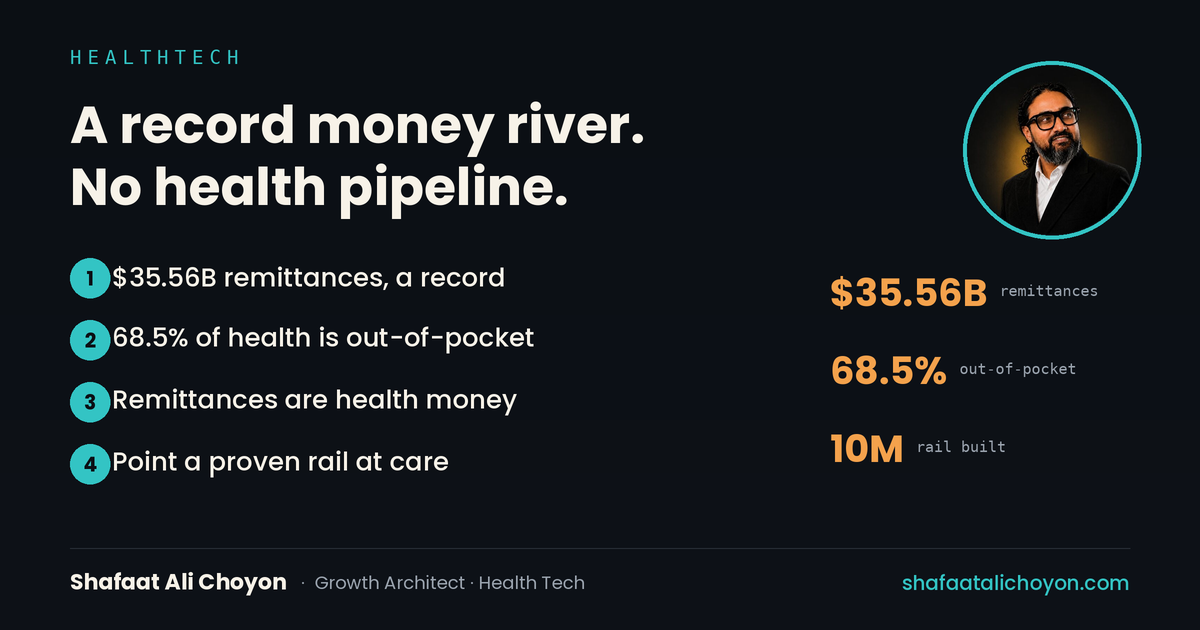

Two numbers sit next to each other in Bangladesh and almost nobody connects them. The first: the country just received a record $35.56 billion in remittances in a single fiscal year — money sent home by workers abroad, much of it to support families. The second: out-of-pocket payments are about 68.5% of health spending, and roughly 70 million people face financial hardship paying for care. One river of money flowing in; one wall of unmet health need. The pipeline between them barely exists.

Remittances are already health spending — just badly routed

Ask any diaspora worker what a chunk of that money is for and a large share will say the same thing: my parents' medicines, my sister's operation, a hospital bill back home. Remittances are already, quietly, one of the biggest sources of health financing in the country — a rail entirely separate from domestic insurance or micro-financing, and far larger than either. But today they arrive as undifferentiated cash — sent, converted, spent reactively in a crisis, with no structure, no pooling, no prevention, and no protection against the catastrophic bill that wipes out a family's savings. It's health money moving through the least efficient possible channel.

This is a fintech-meets-health problem, and I've lived both sides

Structuring that flow is exactly the kind of build I've done. At SureCash we moved government money to roughly 10 million people over mobile rails — distribution to the unbanked, trust engineered in, at national scale. At Praava I ran health delivery — corporate health programs from 342 to about 1,400 clients, diagnostics, prevention as a business. The remittance-to-health pipeline sits precisely at that intersection: take a proven money rail and point it at a proven care system. A diaspora worker in Dubai or New Jersey should be able to fund a parent's health plan back home directly — prepaid check-ups, a diagnostics package, catastrophic cover — not just wire cash and hope.

Why now, and why it generalizes

The timing is real: remittances are at record highs, mobile financial rails are mature, and diagnostics and telehealth in Bangladesh are leaping forward. The missing connective layer is financial. And the pattern isn't only Bangladeshi — remittance corridors into the Philippines, Nigeria, Mexico, and across South Asia all carry the same latent health budget, waiting for someone to give it structure. Build the pipeline in one corridor well and the model travels.

The short version

- Bangladesh took in a record $35.56B in remittances while ~70M people face out-of-pocket health hardship.

- Remittances are already major health financing — but arrive as reactive cash, with no pooling or protection.

- The fix sits at fintech × health, exactly where I've built: SureCash's ~10M-person rail and Praava's care delivery.

- Diaspora-funded, structured health financing is a dual-market opportunity that generalizes to every remittance corridor.

Where is money already flowing toward a problem in your market — just through a channel too crude to actually solve it?

Md Shafaat Ali Choyon (MPH, CHES®, MBA, MCIM) is a growth, marketing and public-health strategist who builds and runs AI in production, with 16+ years across telecom, fintech, e-commerce, consumer tech and healthcare in the US and Bangladesh. See the essays or the portfolio.