Most health-tech pitches start with care — a better app, a smarter model, a slicker clinic. In much of the world, that's the second problem. The first one is money: how a person who has no insurance actually pays for the care in front of them. Solve the payment and the rest becomes possible. Skip it and you've built a beautiful clinic nobody can afford to walk into.

The number that reframes everything

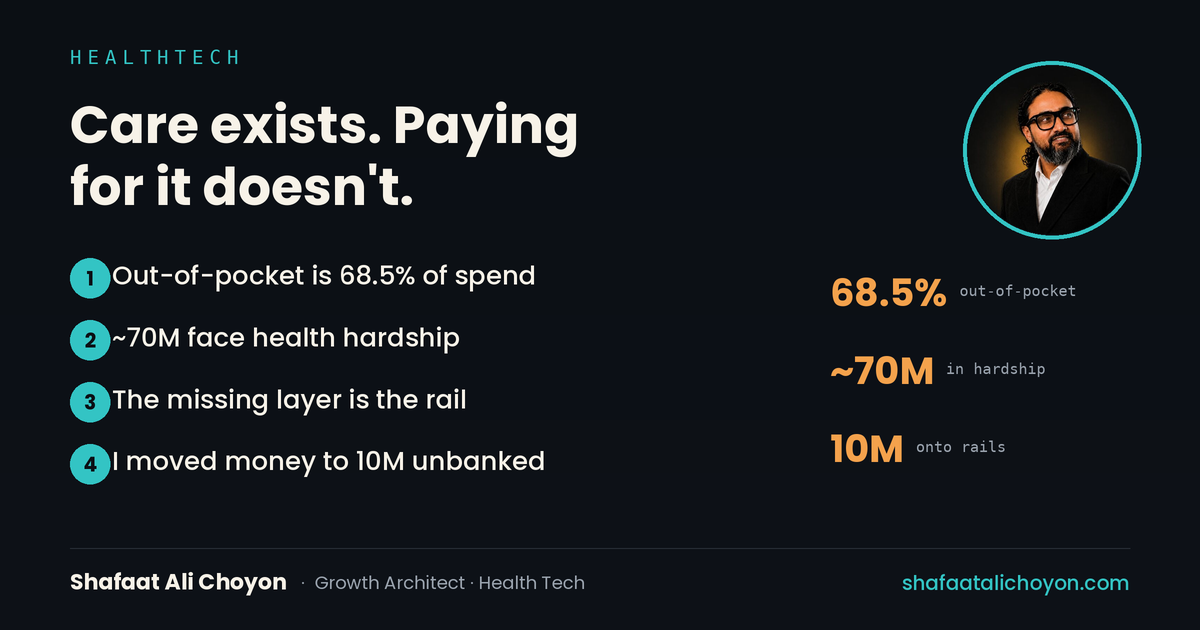

In Bangladesh, out-of-pocket payments make up roughly 68.5% of what the country spends on health — among the highest shares in the world. Around 70 million people face financial hardship because of it, and about one in six patients skip care entirely in a given year because they can't absorb the cost. Formal health insurance covers a sliver: private insurance is a rounding error, and the universal-coverage service index sits near 54 out of 100. Care exists. A way to pay for it, for most people, does not.

The US is drifting toward the same problem

This isn't only an emerging-market story. In the US, high-deductible plans have quietly turned tens of millions of insured people into cash payers for everything under their deductible. GLP-1s bought out of pocket, direct-to-consumer clinics, surprise bills — more and more Americans experience health spending the way a Dhaka family always has: as a sudden, unbudgeted shock. The design problem is converging, from opposite directions.

I've built the rail that's missing

Here's the part I know from the inside. The hard thing about financing the uninsured isn't inventing a new insurance product — it's moving small amounts of money, reliably and trustably, to people the formal system never reached. At SureCash, we put a government stipend into roughly 10 million hands over mobile rails: no branches, no cards, no bank account required. That is the exact muscle health financing needs — distribution to the unbanked, at population scale, with trust engineered in.

What builders should actually build

The opportunity isn't a copy of American health insurance dropped onto a market that can't sustain it. It's embedded, micro, and mobile: pay-as-you-go financing attached to the moment of care, micro-insurance sold in amounts a day-laborer can afford, employer and remittance-funded pools, health savings that live on a phone. Bangladesh's diagnostics and telehealth are leaping ahead; the financing layer under them is still largely unbuilt. Whoever builds it well doesn't just add a feature — they unlock every other health product for the people who need them most.

The short version

- Out-of-pocket payments are ~68.5% of health spending in Bangladesh; ~70M face financial hardship and many skip care.

- The bottleneck isn't clinics or apps — it's the absence of a financing rail for the uninsured.

- I've built national-scale distribution to the unbanked: a stipend to ~10M hands over mobile rails at SureCash.

- The winning products are embedded, micro, and mobile — not a transplant of Western insurance.

If your health product assumed the patient had no insurance and paid cash, what would you have to build first — and are you building it?

Md Shafaat Ali Choyon (MPH, CHES®, MBA, MCIM) is a growth, marketing and public-health strategist who builds and runs AI in production, with 16+ years across telecom, fintech, e-commerce, consumer tech and healthcare in the US and Bangladesh. See the essays or the portfolio.