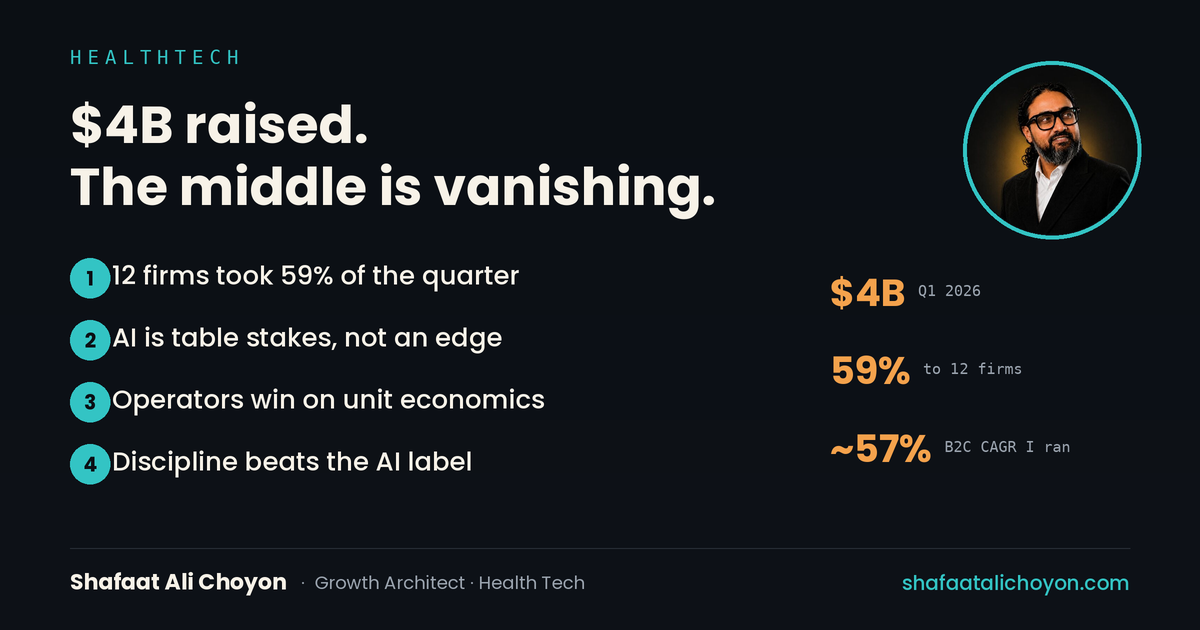

Digital health had its strongest first quarter since the pandemic in 2026 — about $4 billion raised. Read past the headline and it's a more sobering story: roughly 12 companies captured 59% of that money. The middle of the market is being hollowed out, and I've spent enough time as an operator to know what that actually means for the people building.

Concentration is a signal, not a celebration

When a handful of AI-labeled leaders take most of the capital, it's tempting to read it as a boom. It's really a narrowing. Investors are consolidating bets on a few names they believe will win, which means everyone else is raising into a colder, more skeptical room. "AI-powered" has stopped being a differentiator and become table stakes — a box you check to get in the door, not a reason anyone funds you. That reframes the whole game for the other 99% of builders.

What actually wins when AI is table stakes

I ran growth through multi-year hypergrowth at Praava Health — roughly 45% overall and ~57% B2C CAGR across 2021–23, corporate clients from 342 to ~1,400 — and none of it came from a label. It came from unit economics, retention, and building services people would pay for again. That's the operator's edge in a concentrated market: when capital gets scarce and AI is assumed, the companies that survive are the ones with defensible margins and real outcomes, not the ones with the best demo. Discipline is a moat precisely when money is tight.

The dual-market gap widens

US digital health took about 76% of global funding this quarter — the concentration isn't just by company, it's by geography. Meanwhile Bangladesh's healthtech market is climbing from roughly $70M toward $170M by 2027, a fraction of a single US megadeal. That gap is a problem and an opening: the capital-starved market has no choice but to build lean, unbundled, and profitable early — exactly the discipline the flush market is now being forced to rediscover.

The operator's takeaway

If you're not one of the twelve, stop competing on the AI label and start competing on the things a spreadsheet respects: cost to serve, retention, gross margin, and a service customers renew. That's not a fallback for the unfunded — it's the strategy that ages best in a market where capital has become selective and AI has become assumed.

The short version

- Digital health raised $4B in Q1 2026 — but 12 firms took 59%; the middle is disappearing.

- "AI-powered" is now table stakes, not a differentiator.

- What wins is unit economics and retention — I ran Praava to ~45% / ~57% B2C CAGR on exactly that.

- The capital-starved markets are forced into the lean discipline the flush ones now need.

If AI is assumed and capital is selective, what's the number in your business that a skeptical investor would actually respect?

Md Shafaat Ali Choyon (MPH, CHES®, MBA, MCIM) is a growth, marketing and public-health strategist who builds and runs AI in production, with 16+ years across telecom, fintech, e-commerce, consumer tech and healthcare in the US and Bangladesh. See the essays or the portfolio.