Every health system I know is designed for the demographic it had twenty years ago, not the one it's about to have. The fastest-moving force in health isn't a technology — it's the age pyramid, and it's inverting faster than anyone's building for. In the West that story is old news. The part almost nobody is planning for is that it's now happening, at speed, in places that are still poor. Bangladesh is going to get old before it gets rich, and its care systems are nowhere near ready.

The transition is faster than the preparation

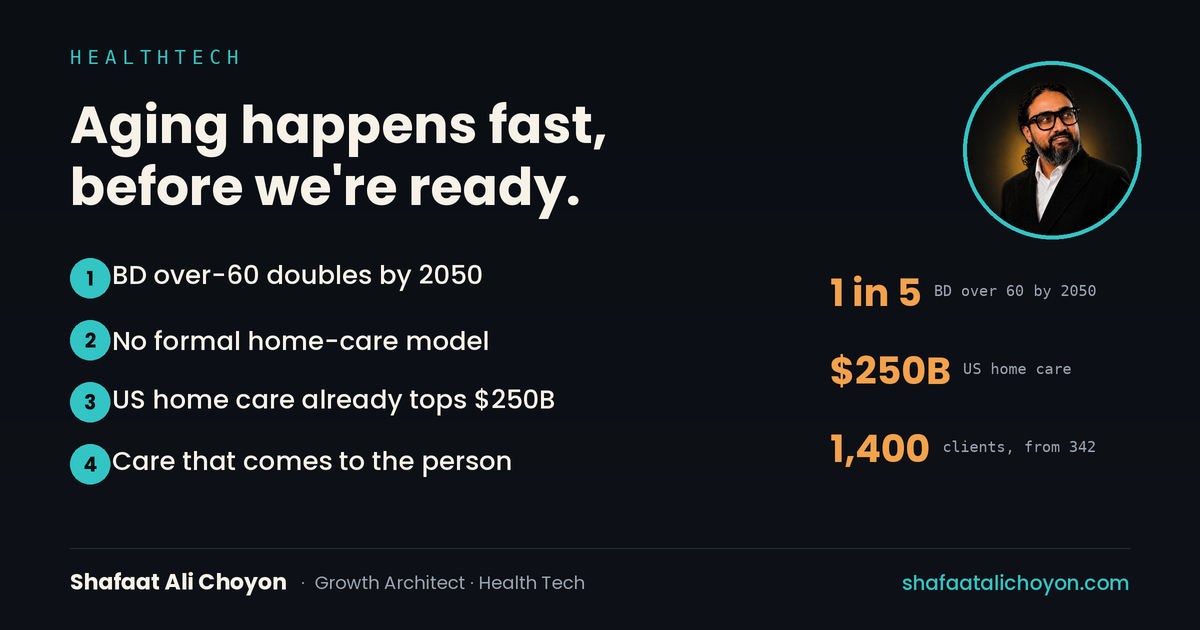

Bangladesh still reads as a young country — but the over-60 share has already climbed from under 8% a decade ago toward roughly one in ten today, on track for one in five by 2050, more than 40 million older adults. And here's the gap that should alarm planners: the country has essentially no formal elder-care model — no established network of home care, assisted living, or long-term care to absorb that wave. The traditional answer, the extended family, is being stretched thin by urban migration and smaller households. A massive need is arriving on a system with almost nothing built to meet it.

The US is the preview — and the market proof

For once, the rich world's version isn't the contrast; it's the forecast. The US home-healthcare market already sits somewhere around $250 billion and is compounding at a healthy clip, driven by exactly this demographic pressure and a clear preference to age at home rather than in institutions. That tells you two things at once: the demand is real and enormous, and the model that wins is care delivered *to* the person, at home, not care that requires them to come to a facility. Bangladesh gets to see its own future in America's present — and to leapfrog straight to the home-based model instead of building expensive institutions it can't afford.

This is the last-mile, delivered-to-the-person model I've built

Elder and home care is, at its core, care that travels to the patient and continuity you can trust — which is precisely the model I've spent years building. At Praava we pushed care outward through home sample collection and workplace and population-scale programs, and grew corporate health from 342 to roughly 1,400 clients by making care reachable rather than making people reach it. Serving an aging population is that same instinct aimed at a new and growing segment: monitoring, chronic-disease management, medication support, and human care delivered into the home, continuously, by people the family trusts. The muscle exists. The market is arriving.

Build it early

The enabling tech is cheap and dual-market: remote monitoring, home diagnostics, medication management, caregiver platforms, and simple check-in systems that let families keep an eye on a parent from a distance. In the US the opportunity is scale and better experience in a market that already exists. In Bangladesh it's building the first formal home-care layer at all, early, while the transition is still underway — the same "design it while the system is still forming" window that closes once habits and institutions harden. Aging is the most predictable trend in health. Almost nobody is building for it early. That's the opening.

The short version

- The age pyramid is inverting fast — including in still-poor countries like Bangladesh, which will get old before it gets rich.

- Bangladesh's over-60 share heads toward ~1 in 5 by 2050 (40M+) with essentially no formal elder-care model.

- The US home-care market (~$250B) is the preview: demand is huge and the winning model is care delivered to the home.

- That delivered-to-the-person, continuity-of-care model is exactly what I built at Praava (342 to ~1,400, home collection).

What demographic shift is arriving in your market on a system built for the last generation — and who's building for it early?

Md Shafaat Ali Choyon (MPH, CHES®, MBA, MCIM) is a growth, marketing and public-health strategist who builds and runs AI in production, with 16+ years across telecom, fintech, e-commerce, consumer tech and healthcare in the US and Bangladesh. See the essays or the portfolio.